Regional PE & Asset Management Market Dynamics

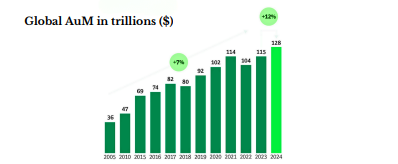

- Global AuM reaches new heights: Assets under management hit a record $128 trillion in 2024, up 12% year on-year, marking a robust rebound from 2022’s downturn

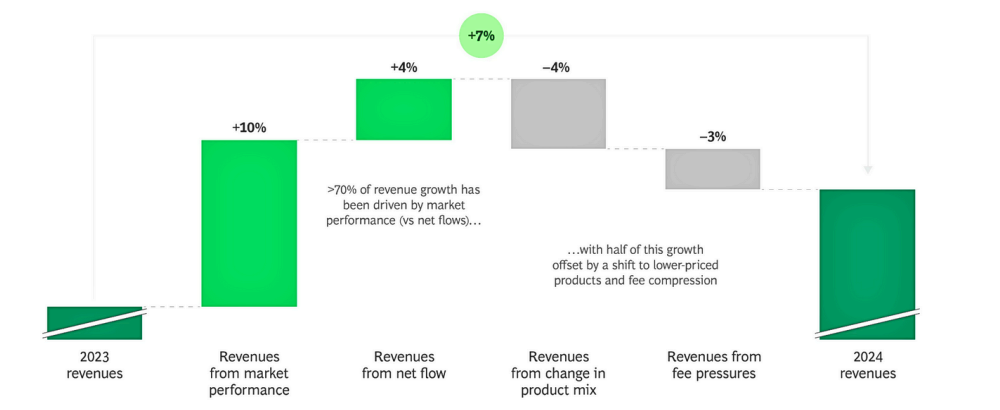

- Revenue driven by markets: Fully 70% of revenue growth in 2024 was market-performance-driven, underscoring persistent vulnerability to external volatility

- Structural headwinds: Margin compression, intensifying competition, and shifting investor preferences toward passive and alternative products are constraining profitability

- United States (Private Equity): Total PE AUM reached $3.128 trillion as of September 2024, the highest since December 2020

Strategic Imperatives for Business Reinvention

Three forces reshaping the industry:

- Product & distribution evolution: Clients demand hyper-personalized, direct-to-investor models.

- Consolidation: Strategic M&A to achieve scale and broaden capabilities.

- Radical cost optimization: Zero-based budgeting and process streamlining for resilience.

Cost-structure trifurcation:

- Investment management & trade execution account for 30–40% of total costs and grew at a 6% CAGR (2022–24).

- Firms now align as “alpha shops, ” “beta factories, ” or “distribution powerhouses, ” each with distinct cost trade-offs.

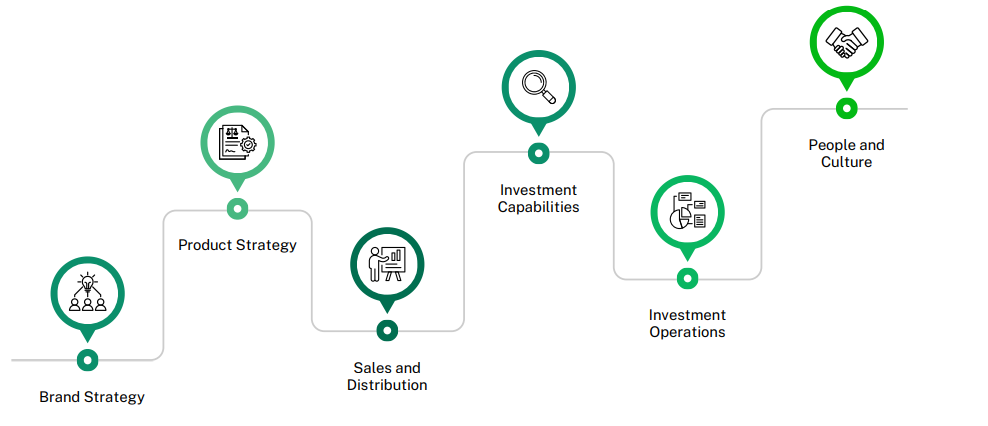

The Six-Pillar Asset Management Blueprint

- Brand: 97% of executives see brand as a critical differentiator.

- Products: 83% are expanding into new investment strategies; 74% pursue hyper-customization.

- Distribution: 91% plan to transform their distribution value chain by 2025.

- Investment Capabilities: AI, analytics, and alternative data fuel next-gen alpha.

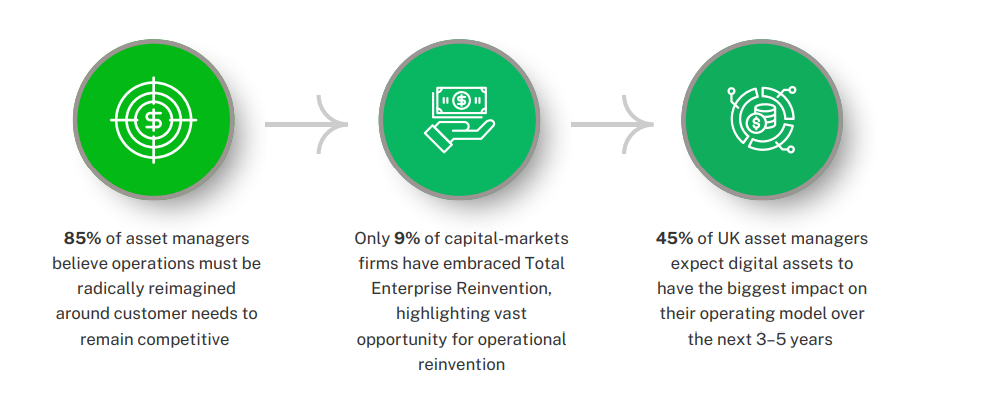

- Operations: 85% believe operations must be radically reimagined for customer centricity.

- Talent & Culture: Blending humans and machines to drive innovation.

AI & Data-Driven Value Generation

Technology as value engine:

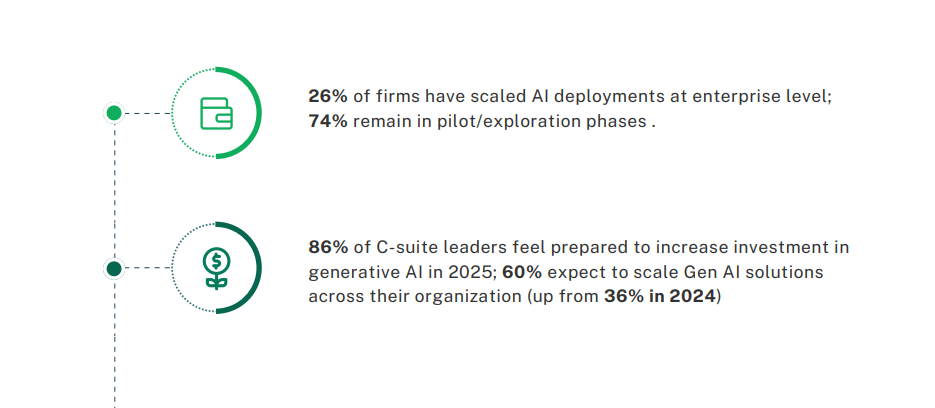

- Only 26% of firms have scaled AI deployments; 74% remain in pilot/exploration phases.

- AI and alternative data at scale expected to shift from experimental to mainstream by 2025.

Active vs. passive flows:

- Passive net inflows outpaced active in 2024, but active strategies show signs of stabilization amid volatility.

PE advantage:

- Private markets’ illiquidity premium and closer alignment of interests provide resilience.

Customer-Centric Operating Model Transformation

Customer-centric operating models:

- 85% of firms say they must radically restructure operations for competitive differentiation.

- Build globally consistent, scalable platforms that embed automation and client-centric processes.

Cost discipline:

- Zero-based cost reviews eliminate redundancies and focus spend on highvalue activities.

PE-specific ops:

- Streamline deal execution workflows, automate performance reporting, and integrate real-time risk monitoring. Adopt cloud-native solutions for fund administration and investor reporting.

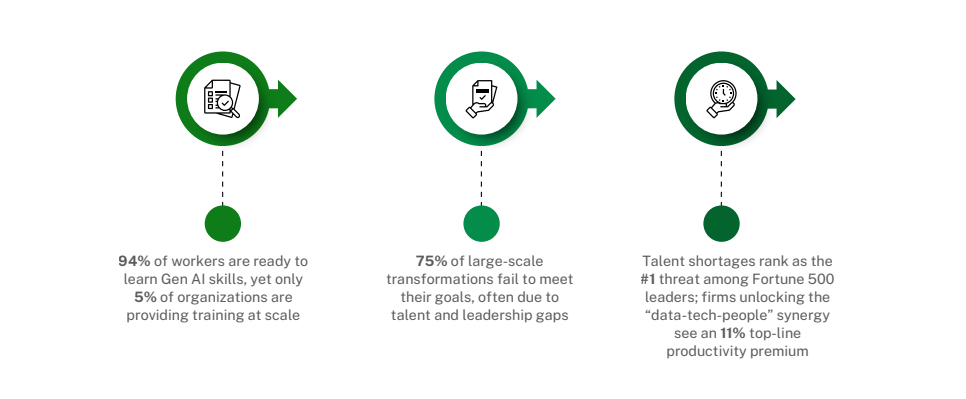

Future-Ready Talent & Leadership Strategies

- Humans + machines: Redefine roles to blend AI augmentation with human judgment.

- Change-mindset culture: Embed innovation in every function; incentivize experimentation and rapid prototyping.

- Develop agile reskilling programs focused on digital, data, and ESG competencies.

- Regional talent strategy: Forge partnerships with Saudi universities and training academies under Vision 2030.

- Attract global talent via PIF-backed initiatives and strengthen in-house digital expertise.

Planning your next acquisition in today ’s volatile markets? Let’s collaborate.